1. A HDB Flat Locks Up All Your Funds

Even if your HDB flat makes you a $10 million profit – there is no way that you can take out these funds unless you sell the flat. There is really no point in feeling satisfied that your HDB flat can make you any profit especially when you are unable to use the money until the moment you sell it away.

In the end, you will still need to consider selling to unlock your funds.

But, if your HDB flat becoming $10 million worth of profits motivates you to sell, don’t you think that selling today and switching to other properties that can give you more potential makes more sense today?

For private properties, you can always go to bank to do a refinancing to take out whatever profits you have made from your property.

Refinancing is impossible through a HDB flat.

2. You Have to Keep Paying Interest on the CPF Funds You Use

Do you know that the CPF interest that you are paying is eating into your cash proceeds?

For example, if you purchase a piece of property using $300,000 from your CPF and today the property is worth $500,000, you cannot get the $200,000 difference in cash.

This is because you need to pay CPF accrued interest using your cash proceeds.

Every year, you are paying $7,500 and more since it is based on compound interest of 2.5%.

So the longer you hold your property, the lesser cash you will be getting back. This will affect the amount of cash you have on hand after you sell in the future if you are looking to upgrade to other properties.

It is because most of your cash proceeds have to go back to the CPF.

Unless property prices keep moving up, do you think the price of your 20 years’ old HDB flat will likewise keep moving up when the government keeps building new flats?

Would you want your children to buy an old HDB flat that is 40 years old or a HDB flat 20 years later when they grow up? Or would you prefer to ask them to buy the newly-built HDB flats?

This will answer the earlier question of whether your old HDB flat price will still increase or not.

3. The Mortgage Servicing Ratio (MSR) is 30% of Your Income

Implemented by the government, this ratio is limiting the potential of the HDB prices. For someone whose household income is $12,000 and who takes a HDB loan at a 2.6% interest rate for 25 years, the maximum monthly installment this family can pay under the MSR is $3600.

What is the price of the property that they can buy using the $3,600 monthly installment then?

Less then $900,000. Pretty low, is it not?

This means that the government is probably going to limit HDB prices to be capped at a maximum of $900,000. Anything higher that that will not get their support.

So a HDB flat at $900,000 should be one that is at the best location. If your location is not the best, you will most likely attract only the lower income buyers which means lower income and lower MSR for you. In turn, this will only limit your property price potential.

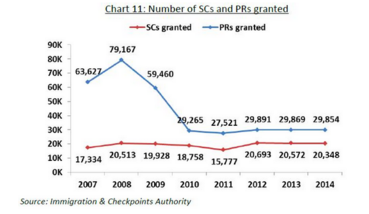

4. Singapore Permanent Residents (SPR) Need to Wait 3 Years Before Buying HDB Flats

Look at the population growth yearly. How many of them are new Singapore Citizens? How many are SPRs?

This means that every year only this amount of people can buy your flat. Simple supply and demand theory. Do you think that your HDB flat price will increase faster then private property?

In 2015, there was a 70,000 increase in the population and only 20,000 qualify to buy your HDB flat.

This means for the rest, they can ONLY buy private properties. Logically speaking, which is better?

Itching to know more before you make your decision?

Contact me and I will dedicate my time and utmost effort to tell you whatever I know.

Additionally, you can also contact your trusted HDB Upgrading Strategist to understand if you need to sell your flat.

Strike while the iron is hot, and you will be the one laughing all the way to the bank.

2 Comments

Juz a average joe interested to get a 2nd property but keeps my HDB. 🙂

Hi KS

Thanks for commenting! Feel free to use the contact form so we can arrange an assessment on your current property portfolio.