Back in August 2016, I met up with this couple who had fully paid their HDB flat in less than 10 years.

They bought their first flat at $400k back in 2008 and now in 2016, it has been fully paid off.

We met up to discuss the process of how they can move forward to buy their next property with his current savings on hand.

The couple has amassed very disciplined and decent savings of almost $200k and wanted to use this amount of money to buy the next property to stay.

The plan is to rent out the current HDB flat to collect rent so allowing them the monthly HDB rental cashflow to pay for the new property. Sounds familiar?

Based on my 10 years as a property agent, I can tell you this is the most common plan that a lot of Singaporeans have.

What if I tell you – this might not be the best plan in today’s Singapore property context?

Let have a look at what will happen if the couple decides to proceed with this plan.

Consequence #1

There will be a payable Additional Buyer Stamp Duty (ABSD) of 7%. For a $1 million property, they will need to pay an additional $70k.

This is a painful amount. Imagine the amount of time that is needed to save up this $70,000 and use it just to pay tax to the government.

For comparison, it can probably pay for the university tuition fees of 2 of your children.

Consequence #2

But wait! Are we forgetting the monthly cashflow we get from renting out the HDB flat?

Assuming the couple rents out the entire HDB flat at $2000 per month, it will take about 35 months to gain back the $70,000. That is almost 3 years!

Also at the same time, it is 3 years of paying out of your own pocket for the monthly mortgage fees of your new property.

The Main Killer To The “Keep My HDB to Rent Out” Plan

The main reason is this terminology that a lot of HDB owners are totally unaware of.

CPF Accrued Interest. This is the main reason that totally killed off their plan and forced the couple to consider other plans instead.

When a HDB property is sold, the sales proceeds will be used to refund the principal amount used as well as the accrued interest into their CPF Ordinary Account.

Let’s just imagine that today, you have already spent $400k from your CPF account to pay off your HDB flat.

ASSUMPTION: On the first day we get the flat, we assume we pay off the full $400K using CPF. If you sell on the 10th year, you will need to return back $112k CPF Accrued Interest more on what you have draw out. The total amount will be $512k.

Using an interest rates table, the usage of $400k multiplied by 1.025 for 10 years and you will get the same amount.

| Year | Accrued Interest Per Year | Total Interest | Balance |

| 1 | $10,000.00 | $10,000.00 | $410,000.00 |

| 2 | $10,250.00 | $20,250.00 | $420,250.00 |

| 3 | $10,506.25 | $30,756.25 | $430,756.25 |

| 4 | $10,768.91 | $41,525.16 | $441,525.16 |

| 5 | $11,038.13 | $52,563.29 | $452,563.29 |

| 6 | $11,314.08 | $63,877.37 | $463,877.37 |

| 7 | $11,596.93 | $75,474.30 | $475,474.30 |

| 8 | $11,886.86 | $87,361.16 | $487,361.16 |

| 9 | $12,184.03 | $99,545.19 | $499,545.19 |

| 10 | $12,488.63 | $112,033.82 | $512,033.82 |

So imagine this – your cash proceeds is never going to be as high as you think it could be.

Yes all the money still belongs to you as it is returned back to your CPF account.

But the CPF accrued interest will easily wipe out any cash gains you think you have.

Ok, then I won’t sell off my HDB flat then!

Assuming you decide to keep the HDB for rental, you do it for the long term.

You accept that $70K is your cost for keeping the HDB flat.

You decide to keep the flat for 30 years.

Guess what? At the end of 30 years, the accrued interest will now be $439k.

| Year | Accrued Interest | Total Interest | Balance |

| 1 | $10,000.00 | $10,000.00 | $410,000.00 |

| 2 | $10,250.00 | $20,250.00 | $420,250.00 |

| 3 | $10,506.25 | $30,756.25 | $430,756.25 |

| 4 | $10,768.91 | $41,525.16 | $441,525.16 |

| 5 | $11,038.13 | $52,563.29 | $452,563.29 |

| 6 | $11,314.08 | $63,877.37 | $463,877.37 |

| 7 | $11,596.93 | $75,474.30 | $475,474.30 |

| 8 | $11,886.86 | $87,361.16 | $487,361.16 |

| 9 | $12,184.03 | $99,545.19 | $499,545.19 |

| 10 | $12,488.63 | $112,033.82 | $512,033.82 |

| 11 | $12,800.85 | $124,834.66 | $524,834.66 |

| 12 | $13,120.87 | $137,955.53 | $537,955.53 |

| 13 | $13,448.89 | $151,404.42 | $551,404.42 |

| 14 | $13,785.11 | $165,189.53 | $565,189.53 |

| 15 | $14,129.74 | $179,319.27 | $579,319.27 |

| 16 | $14,482.98 | $193,802.25 | $593,802.25 |

| 17 | $14,845.06 | $208,647.30 | $608,647.30 |

| 18 | $15,216.18 | $223,863.49 | $623,863.49 |

| 19 | $15,596.59 | $239,460.07 | $639,460.07 |

| 20 | $15,986.50 | $255,446.58 | $655,446.58 |

| 21 | $16,386.16 | $271,832.74 | $671,832.74 |

| 22 | $16,795.82 | $288,628.56 | $688,628.56 |

| 23 | $17,215.71 | $305,844.27 | $705,844.27 |

| 24 | $17,646.11 | $323,490.38 | $723,490.38 |

| 25 | $18,087.26 | $341,577.64 | $741,577.64 |

| 26 | $18,539.44 | $360,117.08 | $760,117.08 |

| 27 | $19,002.93 | $379,120.01 | $779,120.01 |

| 28 | $19,478.00 | $398,598.01 | $798,598.01 |

| 29 | $19,964.95 | $418,562.96 | $818,562.96 |

| 30 | $20,464.07 | $439,027.03 | $839,027.03 |

So 30 years later, in order to make cash from this HDB flat you will need to sell at $839k and above.

Is this really possible? Today if the HDB is 20 years old and 30 years later, it becomes 50 years old.

Can you imagine what will happen to the Singapore property market when a 50-year old HDB flat can sell at $839k?

Most likely this will not happen – no matter how optimistic you are.

Ask yourself – would you prefer to keep something newer that will easily appreciate faster?

Or would you still keep a 50-year old HDB flat?

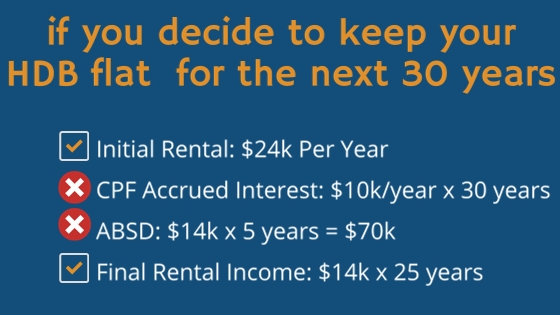

Let’s Fast Forward To You 30 Years Later

Imagine if you sell this 50-years old HDB at only $500k, you would have lost $339k. This would have been your opportunity costs.

Let’s look back at the yearly $24k cash you have collected from the rental of your flat.

About $10k goes to pay off your yearly CPF accrued interest. So now you have $14k/year remaining.

At $14k/year, you will need 5 years to make back your ABSD.

For the rest of the 25 years at $14k/year, you will make $350k.

However in terms of CPF, in the end you will lose $339k.

(FYI: Yes you can choose to APPEAL to CPF Board to NOT pay the $339K accrued interest by asking for a waiver. Based on today’s context, CPF will look on a case-by-case basis. But in 30 years’ time? We won’t be sure.)

Now looking back at this set of calculations – is this really a good investment?

I really don’t know. The perspective depends on how you want to view your CPF, your future home and financial standing in 30 years time.

Maybe putting the $400k inside CPF for 30 years and getting back $839k sounds less risky and less headache for me.

But we must give credit to the CPF system. Only with this system, we can afford to buy a house.

The main question is this: Are we making full use of this system that can have a big positive difference to our end results? A more financially secure retirement and better lifestyle?

The main reason how this couple got to know about this issue is because they chose to meet me to understand their current situation and what are their options available.

I do provide FREE consultation for couples who want to make changes to their property portfolio but are not sure how to go about it.

Imagine you making a decision today NOT to do anything and fully pay off your HDB flat — and thinking you are very safe & free from debt.

30 years later, you choose to sell your house you bought for $400k to cash out for retirement

And then you notice you might need to pay $839k back to CPF.

This is the type of issue that needs careful consideration from knowledgeable property consultants.

Feel free to contact me to understand your current situation now so you can get CLARITY on what to do next.

Only after with the knowledge, then you will know how to protect your assets.

You don’t know what you don’t know.

Sit down and do a thought experiment. Think ahead 30 years in the future. What will that future be like?

And if it relates to your property investment, it is best to sit down and plan ahead with an experienced consultant who has done many similar transactions before.

I like to use the analogy of rock climbing. I have seen how this sport has evolved from extreme sports to becoming mainstream thanks to increasing standards and regulations.

When you go rock climbing, you will find a professional to guide you and all the climbing gears needed to protect you. You won’t just find a rock cliff and start climbing wouldn’t you?

When it comes to property, we also need to consult the professional. This will be a painful experience if you don’t know what to do.

Feel free to contact me if you have questions or wish to review your property portfolio.

P.S You can read another perspective in this Mothership.sg article here.

24 Comments

Hi,

I thought my understanding is that after age 55, you can draw out your CPF money that is above the minimum sum? If yes, isn’t all the accrued interest put back can be drawn out immediately?

Hi Jeffrey you are correct that you can draw out your CPF amount when u are 55 after you set aside the minimum sum.

But when you fully utilize your CPF on your property, you will need to pay a big sum of interest on what you have used.

Example if you use $400k from CPF.

Every year you will need to pay back $10k as interest.

The moment when your property did not appreciate $10k that year – you are actually losing your funds.

Funds you have made on your property previously from a good property market.

So when the property get older and appreciate slower than your interest, then end up you are actually losing a lot of your funds unknowingly.

That is why it is very important to do an assessment regularly – to review the numbers – to make sure you are not losing unnecessary funds without your knowledge.

If the flat is already fully paid for in 10yrs as you have described, why would it still incur accrued interest may i ask?

Hi Lam

The flat was fully paid off using CPF.

This accrued interest is what you would have earned had you not used your CPF for housing. The accrued interest is computed based on the OA savings interest rates applicable during the period that the savings were withdrawn from the OA.

If the flat is sold, you and any property co-owners would use the sales proceeds to refund the principal amount (P) used and the accrued interest (I) into your respective Ordinary Accounts.

Can’t they choose not to sell the HDB at all and pass it down to their kids? In this case they don’t have to “pay back” the accrued interest, yet still enjoy the passive income from rent.

Hi Paul

Yes, you can choose to pass down your flat to your kids.

But it depends on the age of the flat.

If the flat is too old, it might make more sense for them to just get a new flat.

Or perhaps you are thinking of letting your children sell off the flat upon your death.

First, as you continue hold on to the flat, your CPF accrued interest continues to go up. This will deplete any potential cash proceeds.

As your flat start to approach the 99-year leasehold, the price of the flat might not be as attractive as compared to newer flats.

This might affect the future selling price of the flat.

You might enjoy monthly cashflow from renting out but an old flat might not be very attractive.

As accrued interest increases as long as you hold on the flat — you have to decide if holding on to the flat for rental will exceed the accrued interest for CPF.

After 55 CPF still need to retain a fair bit of amount before release and CPF will pay you few hundred monthly not all.

Please proceed to nearest CPF centre to check it out.

As long as using CPF to pay the loan, accured interest will never stop accumulating until the flat is sold.

Please go to the nearest CPF centre to check it out

Pass down to children mean the children cannot apply or buy from market for a flat as well as no condo under their name…

Please ask the agent for more…

I am just a layman, so can only share what I know.

Hi Angie

Thanks for sharing your thoughts. You are right. Unless the children don’t own a flat, then they can inherit the flat.

Otherwise the flat is to be sold upon owner’s death. The thing is – would an old flat with very limited years left on the lease – be an attractive buy in the market?

Hi Angie and Gary,

Firstly is there possibility to opt to pay off accrued interest while holding on to the property (as long as cpf funds are still vested in the property, I believe the clock only simply resets for accrued interest and doesn’t solve the root issue)? other way is to put the money back to cpf (pay back cpf what was borrowed)?

Secondly if the parents will their property to their only child (who owns a private property) the child cannot hold on to the flat (have to liquidate?)?

Thanks and Regards

Hi Will

1) Yes by paying the accrued interest – you only stop the accrued interest from building up. But the principal amount that has been borrowed from CPF still remains AND that interest will continue to build up. That’s why accrued interest will always build up as long as you have used CPF. You have to return to CPF both the principal AND accrued interest – then it stops building up.

2) From my experience, yes the flat will have to be sold upon parent’s death if the child already owns a private property. If you choose to keep the HDB, you will need to sell off the child’s existing private property.

Of course, the best is to check directly with HDB.

So after 10 years, if we sell the

HDB and the funds and accrued interest all goes back to HDB, can we use the money in CPF to refinance and pay for the second property which is still serving loan?

Yes, we can still use the money in CPF to finance for the 2nd property. But the key thing, is how to use our CPF funds wisely in order to make a big positive difference to our end results.

You can request for a free assessment by contacting me.

Hi Gary, thanks for the useful article. Just to check, does your scenario apply to someone who already had $400k in the CPF account and paid off for the flat on the first year? Suppose I had nothing in my CPF, and started paying monthly instalments for 30 years based on my CPF contribution (eg. my OA gets $1.2k per month, I pay monthly instalment of $1.2k from my CPF), will the accrued interest be much less if I pay $400k that way? Thanks!

Hi Yogendran. My article is based on the assumption that you used $400k from your CPF in the very first day you get the flat.

But if you paid monthly installments, the accrued interest will be based on how much you have used so far. I recommend you login to your CPF account and check how much accrued interest has built up.

Make sure you review it constantly as it is based on a 2.5% compounding annual interest. The larger the amount of CPF used, it will result in faster buildup of accrued interest. The moment you finished paying off the loan which is 20-30 years later, that’s when the accrued interest will really start to shoot up. At the same time, your flat is not appreciating as much due to the older age.

Good article to bring insights into the space.

What I’d like to share:

1. Buying ANY properties with loans always need to account for hefty interest charges, not just HDB.

2. Author’s assumptions point to potential worse off situation if holding on to HDB for too long, that I also agree. In fact, assuming all else status quo, any properties that are 99-year leasehold face the same problems. Leasehold private properties or any ‘asset’ for that matter always face a time decay: logicallly owner can’t sell for higher. Accounting 101: (freehold) land/real estate does not have depreciation charges that leasehold properties do. But for some strange reasons, this premium is not priced reasonably in the housing markets by the majority of participants.

3. However, author has not yet addressed the issue suggested by the article headline. Suppose same example cited but now with owner selling the HDB, even at sweet-spot time frame of <15 years since TOP, then ploughing all proceeds, after covering CPF loan, into a new property, at a HIGHER valuation & loan quantum. The owner could save the ABSD. But net-net, owner would still be stuck in the same situation: a mortgage loan from either CPF or bank, this time much bigger! What the owner just did is simply rolling into a new(er) place with bigger loans; same problem, just bigger now.

There are many ways to invest in properties.

If people wish to profit from capital gains, then flipping new, leasehold properties could be the most ideal in a RISING market: low % down, no hefty interests over time, relatively high ROI. I emphasise on the word 'rising' as the contrary could kill. High turnover generally a boon to all participants, but best for 'flippers', agents, lawyers, developers, banks, land authorities etc just to name a few. So, please be careful whenever someone advises you to buy/sell anything, because you never know who's fleecing you. But this is bad collectively for the overall health of the market for the masses as high churn likely leads to fast-rising prices. Hence the Seller's Stamp Duty from government starting a few years back.

Alternatively, we could also approach the market from the rent- or cash flow-seeking perspective. As long as the properties are generating healthy cash flows that more than enough to offset the mortgages, it is an asset, regardless of the growing liabilities. To someone who's more risk-averse, imagine if the person bought the 400k flat and serviced it with CPF loan. At the end of 30 years, less valuable property on paper vs higher CPF liabilities. But it shouldn't bother the person as it's still owner-occupied. The owner could rent out parts of the flat to service other needs, even perhaps some investments that make better returns. Imagine a REIT that has long term sustainable DPU profile. That's easily more than 2.6% of the CPF loan in current situation. However, like all investments, there could be risk of losing capital. But hey, the money being invested comes from the positive rental cash flows, remember? This person may have big liabilities, but is able to have more money to eat, buy groceries, travel or maybe invest further. Vs the person who's rolled into a single, bigger property with bigger mortgages to service, this owner seems better off to me.

In short, investing in real estate, or anything for the matter, is tricky at best and nightmare sometimes. It's best to discuss more with different people as suggested by the author to get different perspectives. There's no one-size-fits-all. When it comes to the decision to buy a second or multiple properties, my 2-cents-worth is: don't stretch it. Always work with less rosy scenarios into the future to see how sustainable servicing those mortgages can be. For someone who's wealthy like Mr Wee Cho Yaw, that just bought many units at Nassim, why not? But for most of us, always assume the worst and make sure we have not one, not two, but many, multiple layers of interest cover in case of bad weathers before we make the leap.

Hi Wei Sing. I agree with your main points.

Yes, we are going into a bigger loan and bigger investment.

That when we need to choose the correct investment to make sure this investment grows faster then our accrued interest.

Most importantly, we restructure and “reset” our CPF usage.

Example a fully paid HDB at $400k. Every year, the accrued interest on average is about $10k.

For a $1m property with a full 80% leverage, the CPF usage of $150k will have accrued interest of $3750.

Which property has a higher chance to appreciate that can cover the accrued interest?

A $400k HDB to grow by $10k or a $1m property to grow by $3750?

Of course: there is no right or wrong answer. Everybody has their own unique situation and this might not be for everyone.

But ultimately – it is more important to regularly review your finances and know exactly what are all your funds are doing.

Hi, take it that hdb is fully paid and u sold it later and understand as mentioned by you we need to put back acurved interest. Would’nt it be the same the cash goes inside our cpf? Correct me if I’m wrong.

Hi Mr Chan

Yes, the accrued interest will go back inside your CPF account. The problem arises when there is a possibility the accrued interest exceeds the selling price of the flat. It can result in a “negative cash sale” situation.

Hi Gary, if a couple don’t sell their flat until their death, and the property is inherited by their child, when the child sell off the property, does he need to pay back the accrued interest to CPF?

Hi Eva

No, accrued interest is not payable as the CPF used was from the deceased CPF accounts. So all proceeds will be received as cash as it considered as the deceased’s CPF account as closed.

Hi .

My dad and I owned our flat since 1995 and it is fully paid off. While he paid the monthly mortgage in cash, I paid for it using my CPF except for the last 12 years. (My dad continued to pay for it in cash)

My parents are over 70 and we plan to sell the flat, hopefully within the next 1-2 years, as they plan to migrate and join me. How does that work and would you have any advice. Thanks in advance.

Hi Lorietta

Upon selling the flat, a certain portion will go back to CPF (since you have used CPF). But your accrued interest is not likely to be very high as you have paid a certain portion by cash.

You can go through the normal sales procedure – http://www.hdb.gov.sg/cs/infoweb/residential/selling-a-flat/selling-process/timeline

https://www.facebook.com/notes/cpf-board/8-things-you-should-know-when-using-cpf-for-property/10154443613615177/?pnref=story

You and your co-owner do not need to top up the shortfall in cash as long as the property is sold at or above its current market value.

Hi Daryl

You are right. Based on the FB comment thread, the current market value will be based on the current valuation of the flat.