Being a property agent for the past 10 years, I have encountered many different issues and stories that the Singaporean home owner faces.

I have dealt with various property issues that run the entire spectrum – from straight up losses to massive windfalls. I encountered young couples, middle-aged couples, broken-up couples, business owners, budding investors and of course retiree couples.

These encounters have deeply enriched my experience and knowledge as a property agent. Here I like to share with you the phenomenon of the older retiree couple.

The Phenomenon of the Downgrading Retiree Couple

The retiree couple is easily identifiable – they consist of a husband & wife in their late 50s or early 60s – whom both are no longer holding a full-time job. They are likely to be living in private property.

Their children are grown up and working – some still live with their parents while others might have moved out.

Where will you be in 30 years’ time?

Most meet up with me to sell their existing private property so they can downgrade to a HDB flat. They are more common than you think.

Why are they downgrading? The reason is very simple – to unlock their retirement funds.

They have been diligently paying their monthly installments and over the years, the value of their private property has appreciated.

Whatever gains the property has made – well… that is going to be part of their retirement funds.

By downgrading, they are able to extract their funds. After selling off their private property, the retiree couple will usually buy a HDB flat from the open market.

They are unlikely to go for BTO flats because some of these locations have little amenities or are less developed. The smaller concentrations of wet markets or medical clinics makes these new BTO launches less desirable.

Convenience of staying near mature HDB estates

Their choice of a convenient HDB flat will be very reflective on their new lifestyle as retirees:

- Near to the supermarkets – preferably walking distance. Walking is their main mode of “transportation”. Convenience is key!

- Near to their children’s home

- Near to parks or amenities they can explore

- Far away from the central regions or city fringes

- More mature HDB estates

Such choices are available to them – thanks to the proceeds from the sale of their private property.

What (other) Choices Are Available To The Retiree Segment?

In Singapore, reverse mortgages are not available for the private property segment.

For those living in HDB, there is an option of the Lease Buyback Scheme. However this option is only open to those living in 4-room HDB flats or smaller. The most important thing to take note regarding Lease Buyback Scheme is the portion below:

The most significant point of note is that the value of the participatory flats are determined and fixed at the time of enrolment. It does not take into account any future appreciation over the lease period, but only straight-line depreciation. This is an unlikely occurrence in land-scarce Singapore where a high demand for housing constantly drives the property market.1

Basically, the value of the flat is fixed at the time of enrollment. The value will also be considered to depreciate in a straight line – not taking account of any appreciation. The remaining lease of the flat that is sold back to HDB should also be at least 20 years.

The other alternative is to sell your existing HDB flat and downgrade to an even smaller flat to extract retirement funds.

Are you willing to compromise on your lifestyle during your retirement to live from 4/5-room HDB flat to a studio/2/3-room HDB flat?

(To extract larger funds, you need to make larger “downgrade” – perhaps all the way to studio HDB flat. This depends on each person’s individual situation.)

Making A New Choice In Your 30s

One of Stephen Covey’s key 2nd habit from “7 Habits of Highly Effective People” is to Begin with the End in Mind.

These retirees made an additional choice in their younger days. They made a choice to upgrade to private property decades ago – in spite of their busyness of working and raising their families in that period. They decided to begin with the end in mind.

In a way, this is like the housing cycle completed – from HDB to Private Property and back to HDB.

A potential option to downgrade is available – if you upgrade to private property earlier in your life.

In the process, this resulted in a “retirement savings plan” that was locked within their property.

By upgrading to a private property in your 30s, it is much more affordable as you are able to get a longer loan repayment period – thereby resulting in smaller monthly installments.

Of course, this option only comes to you once in your 30s – your peak income & longer loan period.

As you cross your 30s into your 40s, your property choices become more limited.

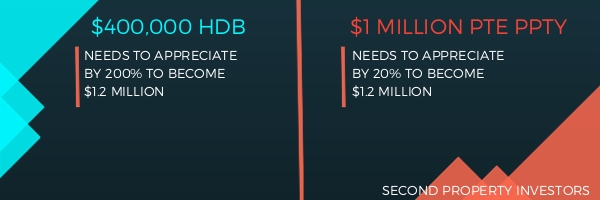

Rate of Appreciation of HDB Vs Private Property

The key factor in property investment is the passage of time. As time marches forward, let’s see the impact of property values on both HDB and Private property.

Let’s Fast Forward to 30 Years Later:

Which is the more likely scenario? A HDB flat appreciating by 200% or a private property appreciating by 20%?

When you make an additional choice in your 30s, you have the opportunity to make another choice in your 50s. That is the choice to downgrade from private property back to HDB.

What if you choose not to upgrade to private property? Then it is likely to downgrade to a smaller HDB home in your retirement.

With an upcoming supply of 17,000 flats coming up the pipeline, HDB flats are unlikely to appreciate by a lot more.

In the past about 30 – 40 years ago, prices of HDB flats were extremely low and it was the norm to see prices of flats appreciate by 3-4 times.

In contrast, presently – the prices of flats of new flats purchased in the past 10 years ago have only appreciated by less than half.

Engineering Your Retirement Now For More Choices In The Future

For these retirees, a downgrade from private property to HDB is not really a downgrade.

Because technically, they would have reaped good returns with a nice pile of cash AND a fully-paid for HDB.

After 30 years of paying your monthly installments, there are 2 choices that you can have:

- a fully-paid $500K HDB flat or

- a fully-paid $1 million condo

With a $500k, 30 years old HDB – what are the other choices you have to cash out?

- Sell the HDB flat and stay with children?

- Or sell and move to smaller and older HDB flat that “should be” cheaper?

The alternative choice is a $1 million condo that you can sell…. and change to $500k HDB flat AND have $500k on hand. (That would potentially be a nice retirement plan.)

So the key thing – how can you afford to upgrade when you are STILL YOUNG?

With the correct strategy and financial knowledge, you can do it easily without any stress.

Many of my clients has successfully done it.

So the choice is yours.

In 30 years time, which property do you prefer to own…. WHEN it becomes fully paid?

You are welcome to contact me for a no-obligation consultation if you have bought your HDB flat before 2011-2012.

Read also: Your Primary Residence – Is it a Home or an Investment?

![How Long Can Your BTO Flat Value Last? [Examples Included]](https://www.secondpropertyinvestors.com/wp-content/uploads/2019/03/bto-flat-value-150x150.jpg)

Leave a Reply